Forty-plus years later, investors and advisors have seemed to embrace the “owning the haystack” philosophy, most likely due to decades of evidence on the case for low-cost market-cap-weighted indexing. This transformation resulted in an unprecedented rise in market share for indexing as the core of most portfolios. At the same time, the distinction between what is labeled active versus index became less clear, and many now use index funds “actively,” which together, resulted in a “blurring of the lines between index and active,” rendering the distinction and the debate between them much less relevant.

Today it is highly likely that most, if not all, investors own every needle in the haystack to some degree or another. Thus, the focus has shifted from merely owning the haystack to understanding the critical importance of the relative weight of each needle within it. This nuanced understanding emphasizes that managing the weight of each needle—each security's market cap weighting—plays a crucial role and reflects the collective risk and return expectations of all market participants at any given moment. The dynamic nature of market prices, as they seek to balance buyers and sellers in transparent auction markets, highlights the challenge of outperforming a market consensus that is shaped by numerous well-informed investment professionals, along with the paradox of skill.

Given the above developments, a modernized interpretation of Mr. Bogle's advice would be, “Own every needle’s market weight.” In other words, since each needle is likely in the portfolio, Mr. Bogle’s advice to own every needle has largely occurred; and it is now the weighting of each needle at the total portfolio level that is most critical to long-term client outcomes.

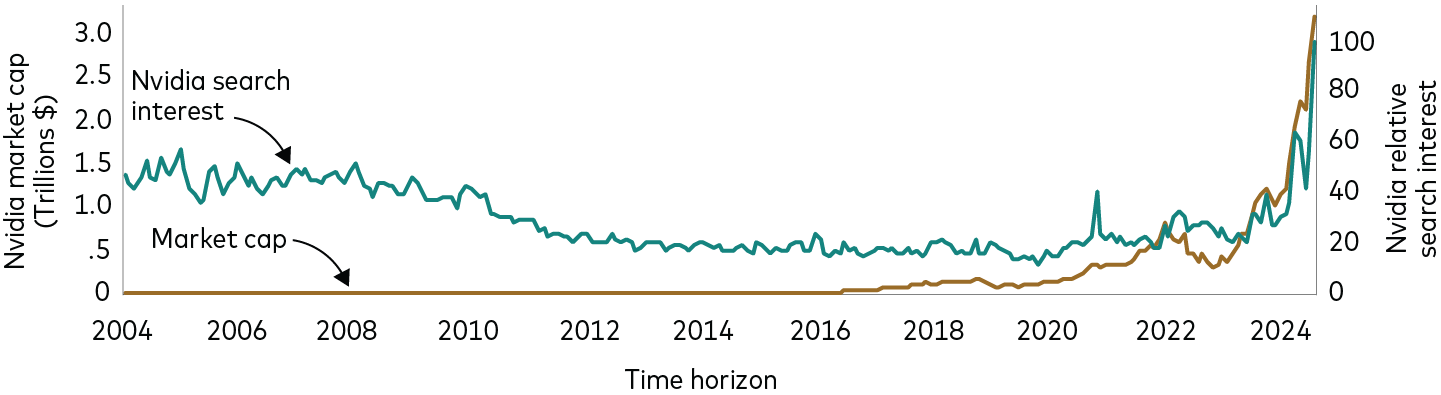

With the above context, perhaps the weighting of each needle has never been more important. For example, using the current market as a guide, as of June 26, while the U.S. equity markets are up approximately 3%–5% for the quarter and 13%–15% for the year, returns continue to be concentrated in large-cap U.S. growth stocks, specifically, Nvidia and the Mag 7.1 The most recent headlines have centered on Nvidia surpassing Microsoft as the most valuable public company in the U.S.2 as well as surpassing the entire market capitalization of large global economies, such as Germany, the U.K., and France.3 As Nvidia’s market cap increased, so did awareness of the company as demonstrated by Google search interest in Nvidia seen in Figure 1. For much of the past two decades, search interest in Nvidia and public awareness of the company was a tiny fraction of its current peak, only accelerating over the past 18 months as the company’s market cap skyrocketed from around $300 billion to more than $3 trillion.

Figure 1: Nvidia Google relative search interest and market capitalization since June 2004

Source: Vanguard Investment Advisory Research Center calculations data from Google, Inc., and FactSet as of June 18, 2024.

Notes: We computed relative searches for Nvidia over the course of a 20-year period. Each number is in relation to the relative highest popularity, 100, which occurs after January 2024, implying peak popularity within the past 20 years.

So why does this matter? Because the tremendous growth and success of Nvidia can only be seen in hindsight. Choosing a company that has a high likelihood of outperforming in the future is akin to finding the needle in the haystack. The risks of missing one, or even a few, of the subset of stocks that have historically driven market returns are obvious, especially given how hard it would have been to own them all through any product other than a broad-based market-cap index fund. Complicating the challenge is that once the growth and interest in the stock has accelerated, it can be difficult to jump in when the headlines may be advising otherwise.

Hindsight is 20/20

In 2024, it seems completely obvious that investors and/or their advisors should not have underweighted Nvidia given its tremendous success. But was this as obvious 20 years ago when its market cap was less than $5 billion or even as recently as September 2022 when it was close to $300 billion? Many members of the Mag 7, or as we like to reference the Magnificent 84 (Mag 8), have endured plenty of naysayers along their paths to success. For example, Apple was on the brink of bankruptcy when it battled back to replace BlackBerry as the market leader for smartphones. Microsoft was long a bellwether in value indexes before the emergence of its cloud business. Many wondered if Netflix could replace Blockbuster and transition into a streaming powerhouse. There are similar examples for Mag 8 companies Tesla, Alphabet, and Meta as well as other companies if we look further back into history with the equity markets, such as the emergence of IBM or the energy stocks in the '70s and '80s. While this time, the names are different, the benefits of owning the haystack through time have been powerful, as seen in how hard it has been for active managers to outperform market-cap-weighted index funds. In the end, the highest probability of ensuring exposure and the market-cap weights to the future top-performing companies while not knowing in advance which companies these will be is to own the haystack; that is, the market-cap-weighted portfolio.

Risk of not owning the haystack

The consequences of underweighting or not owning the best-performing needles in the haystack can be significant. While investors and advisors are well aware of this, the headlines over the past decade have repeatedly suggested that the Mag 7 is overvalued and likely due for a pullback. As a result, the temptation to underweight these companies has been high, which is understandable given their valuations and the fact that trees do not grow to the sky. We also know that market leadership is cyclical and can include large movements on a given day; however, the timing of such cyclicality has remained highly elusive and thus can adversely affect client and practice outcomes. Although it can be difficult to tune out the noise, rather than react to the noise, our 3B Mental Model has helped advisors and their clients “stay the course.”

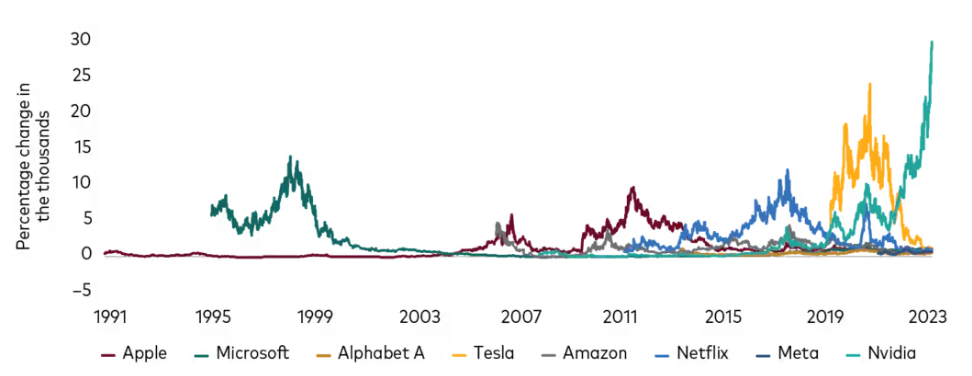

The risk of reacting to the noise is the potential to miss out on remarkable returns which only come to light after the fact. Each of the Mag 8 stocks has gone through a period of exceptional 10-year returns as seen in Figure 2, which shows the rolling 10-year returns for each of the Mag 8 companies since 1991.

In this illustration, one can easily pinpoint the period during which each company had its best 10-year return and the relative magnitude of that return. This once again reinforces the power of owning the haystack—and the needles in their market-cap weightings—as performance leadership among these companies has been cyclical, extreme, and hard to predict in advance. Figure 2 also shows, with Nvidia, we are witnessing history as its current 10-year trailing return is the largest among this magnificent group at 29,988%, surpassing Tesla’s January 2022 return of 24,170% and Microsoft’s April 1999 return of 14,001%.

Figure 2: Rolling 10-year percentage change of Magnificent 8 stocks since 1991

Past performance is no guarantee of future results.

Source: Investment Advisory Research Center using data from FactSet, Inc. Data as of June 21, 2024.

Notes: The above figure shows the rolling 10-year cumulative total returns of the Magnificent 8 securities on a daily basis since January 1, 1982. The Magnificent 8 stocks include Nvidia, Microsoft, Apple, Alphabet, Amazon, Meta, Tesla, and Netflix. Note—the fact that the Mag 8 and Nvidia have had this performance in the past is no way an endorsement of their future prospects, but rather is a reminder of the risks of underweights relative to the market-cap-weighted portfolio—and is backward looking. The future is uncertain, and we have no idea what will happen to Nvidia or the other Mag 8 stocks, but we do know deviations from the market-cap-weighted portfolio will create deviations from the benchmarks that clients use to evaluate the performance of their portfolio and their advisor. The fate of these companies, as always, will be determined in the future by their revenue, margins, competition, and market valuation multiples.

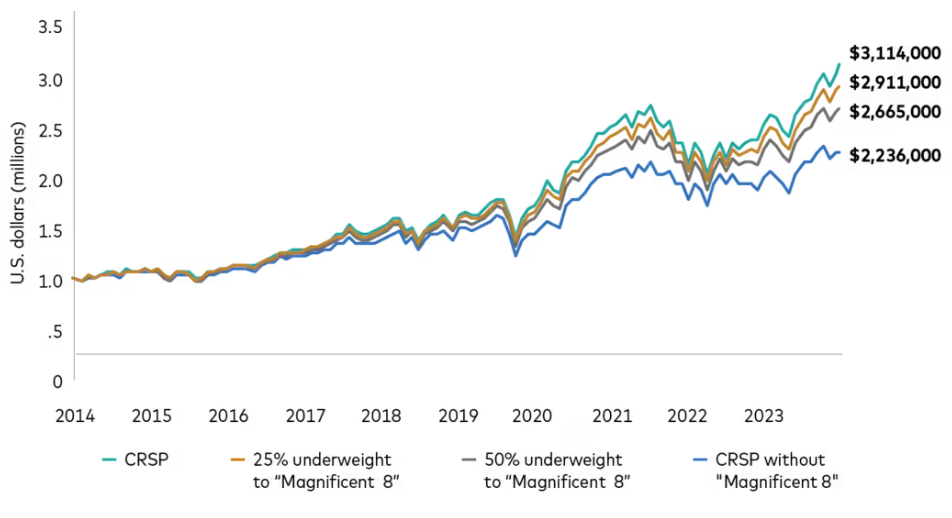

While it is unlikely for investors or advisors to have had no exposure to the Mag 8 over the last decade, even a modest 25% relative underweight5 can have a significant impact on client and practice outcomes. For example, a $1 million investment in the U.S. market-cap-weighted portfolio in June 2014 would have grown to $3,114,000 through June 18, 2024. A 25% underweight to the Mag 8 would have resulted in a $200,000 deficit, a 6.5% relative underperformance to the broad market portfolio as seen in Figure 3.

It would not be surprising for clients to question the underperformance created by such underweights and to potentially seek a new advisor as a result. Therefore, owning the haystack is not only a powerful benefit to your client wealth outcomes, but equally as powerful to your practice outcomes, as client retention and portfolio churn rates are highly critical to the success of the advisory practice in an increasingly fee-based world. The advisor community is exponentially gravitating to this philosophy as evidenced by, the unprecedented rise in broad-based indexing market share in portfolios, increased usage of core market-cap-weighted ETF model portfolios, and the wide scale movement to a value proposition as articulated in Vanguard’s Advisors Alpha® framework.

Figure 3: Relative underweights to the Mag 8 trailed the broad market by wide margins

Past performance is no guarantee of future results. The performance of an index is not an exact representation of any particular investment, as you cannot invest directly in an index.

Source: Investment Advisory Research Center using data from FactSet, Inc. Data as of June 18, 2024.

Notes: The above figure shows the value created of an initial, hypothetical $1 million investment in the CRSP U.S. Total Stock Market Index, along with 25%, 50%, 100% relative underweights to the Magnificent 8 stocks since June 30, 2014. The Magnificent 8 stocks include Nvidia, Microsoft, Apple, Alphabet, Amazon, Meta, Tesla, and Netflix.

The best thing advisors can do for their clients is to produce great investment outcomes. By owning the haystack, advisors give their clients the highest probability that they will have market-cap weightings that are derived by the consensus of all investors and have historically been a very tough benchmark to beat. Perhaps equally—if not more important—is engaging with clients and building trust. There will always be uncertainty in markets and headlines encouraging clients and advisors to engage in trading that may not be in the best interest for clients’ investment success.

And this quarter is no different. Your clients have most likely been overloaded with information on the Mag 7 , Nvidia, and varied opinions on the potential portfolio implications. This provides a great opportunity for advisors to engage with their clients and build upon the trust they have established. By leveraging history as a guide, advisors can remind clients that concentration within the returns of the equity markets is nothing new—a small percentage of companies have been responsible for half of the equity market returns over the past nearly 100 years. Help them understand the benefits of owning the haystack and each of the needles in their market-cap weights. And finally, help them to tune out the noise. By doing this, your clients and your practice have the best chance for long-term success!

1 The term Magnificent 7 (Mag 7) was coined in 2023 and includes: Apple, Microsoft, Amazon, Alphabet (Google), Meta (Facebook), Nvidia, and Tesla.

2 Wall Street Journal, 2024. Nvidia Tops Microsoft to Become Largest U.S. Company. June 18; available at www.wsj.com

3 CNBC, 2024. Nvidia tops the individual stock market values of Germany, France, and the UK. June 20; available at www.cnbc.com

4 Prior to the Mag 7, there was FANG (Meta [formerly known as Facebook]; Amazon; Netflix; and Alphabet [formerly known as Google]) in 2013, which became FAANG in 2017 with the addition of Apple. When analyzing the past 10 years, we think it is important to include Netflix and therefore refer to the group of companies as the Magnificent 8 (Mag 8).

5 In other words, if the Mag 8 accounted for roughly 27% of the index as of May 31, 2024, the 25% underweight allocation would be approximately 20%.

Notes:

All investing is subject to risk, including possible loss of principal.

Be aware that fluctuations in the financial markets and other factors may cause declines in the value of your account. There is no guarantee that any particular asset allocation or mix of funds will meet your investment objectives or provide you with a given level of income. Diversification does not ensure a profit or protect against a loss.

Past performance is not a guarantee of future results.

CFA® is a registered trademark owned by CFA Institute.

Vanguard Mexico is not responsible for and does not prepare, edit, or endorse the content, advertising, products, or other materials on or available from any website owned or operated by a third party that may be linked to this email/document via hyperlink. The fact that Vanguard Mexico has provided a link to a third party's website does not constitute an implicit or explicit endorsement, authorization, sponsorship, or affiliation by Vanguard with respect to such website, its content, its owners, providers, or services. You shall use any such third-party content at your own risk and Vanguard Mexico is not liable for any loss or damage that you may suffer by using third party websites or any content, advertising, products, or other materials in connection therewith.